By Mu Li, CPM Group

On the eve of the new President’s inauguration, 50 MMTA members and friends met for this year’s sell-out New York Dinner, to kick off the New Year. Increased optimism was definitely in evidence from many, both in terms of the first couple of weeks’ business, and also in anticipation of the new Administration.

Following an animated networking reception, CPM’s Mu Li offered an outlook on planned policy shifts that are expected to affect commodity markets, and what these shifts could mean for both the global economy and for commodities.

How we arrived at this point

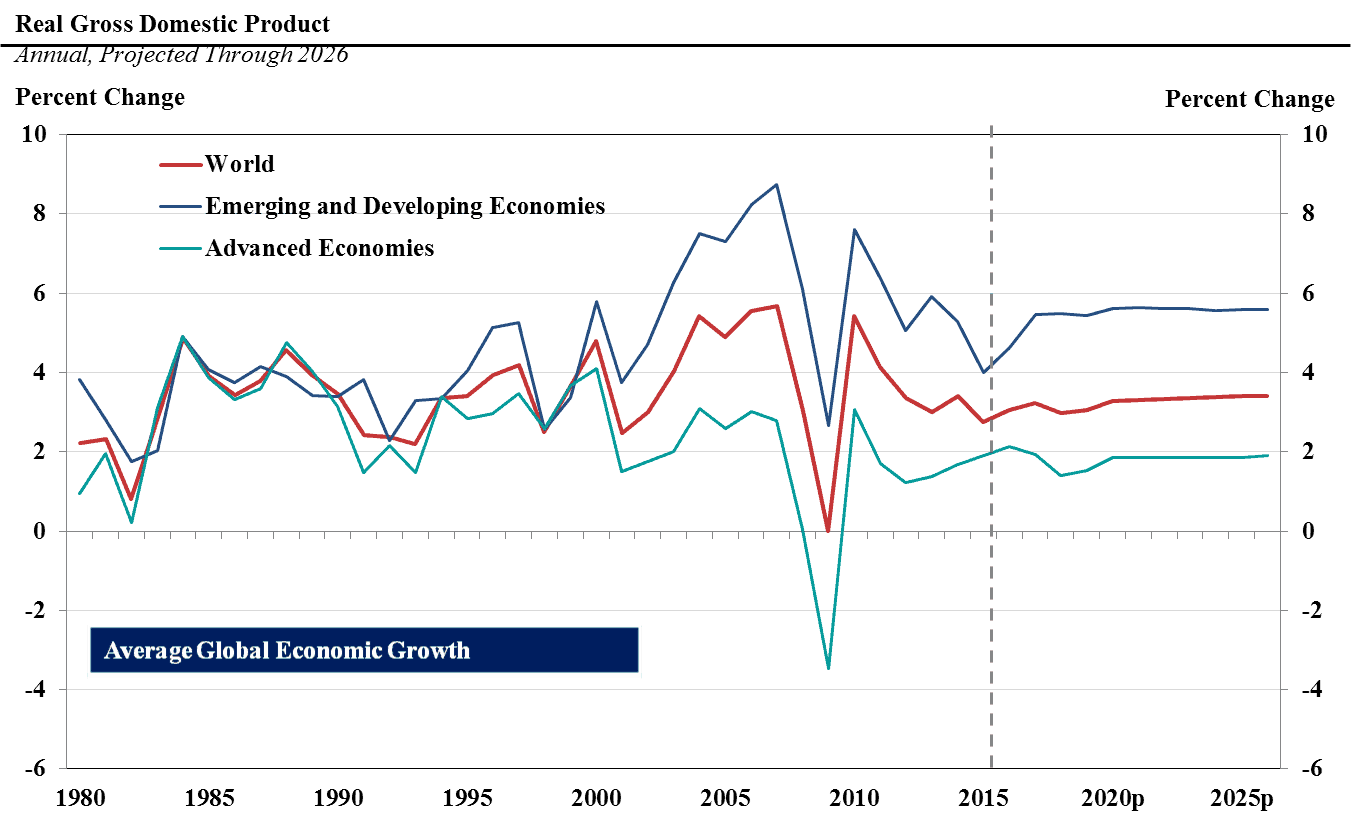

It is clear that there is dissatisfaction globally regarding political and economic conditions, and increasing income disparity and anemic growth following the Great Recession have only intensified this dissatisfaction. Recovery from the recession has been one of the slowest in history; uncoordinated monetary and fiscal stimulus around the world have resulted in rolling recessions across the developed economies, which eventually poured into the growth of developing economies, depressing growth over the past few years. Problems began in the developed economies, and while the larger developing economies were able to shelter themselves from the problems initially, the ongoing weakness of developed economies finally began to have a negative effect on developing economies as well. In developed economies, cautious use of debt by consumers and lackluster wage growth are all factors that weighed on economic growth. These factors have led to increasing frustration and anger, resulting in votes for change in both the UK (Brexit) and US (Trump). In CPM’s opinion however, this anger and frustration are misplaced, with structural changes in developing economies, such as aging populations with different consumption patterns, and the increased use of computers to replace low skilled labor, being important factors that have been underestimated. Globalisation, they believe, has helped raise large swathes of the global population into the middle class.

“In industrialized economies structural changes and aging populations suggest relatively slower growth is the norm to be expected. Capital constraints in emerging economies resulting from capital flows out of these countries into Western financial markets are likely to intensify going forward.”

Surplus labor will be a major global problem now and going forward

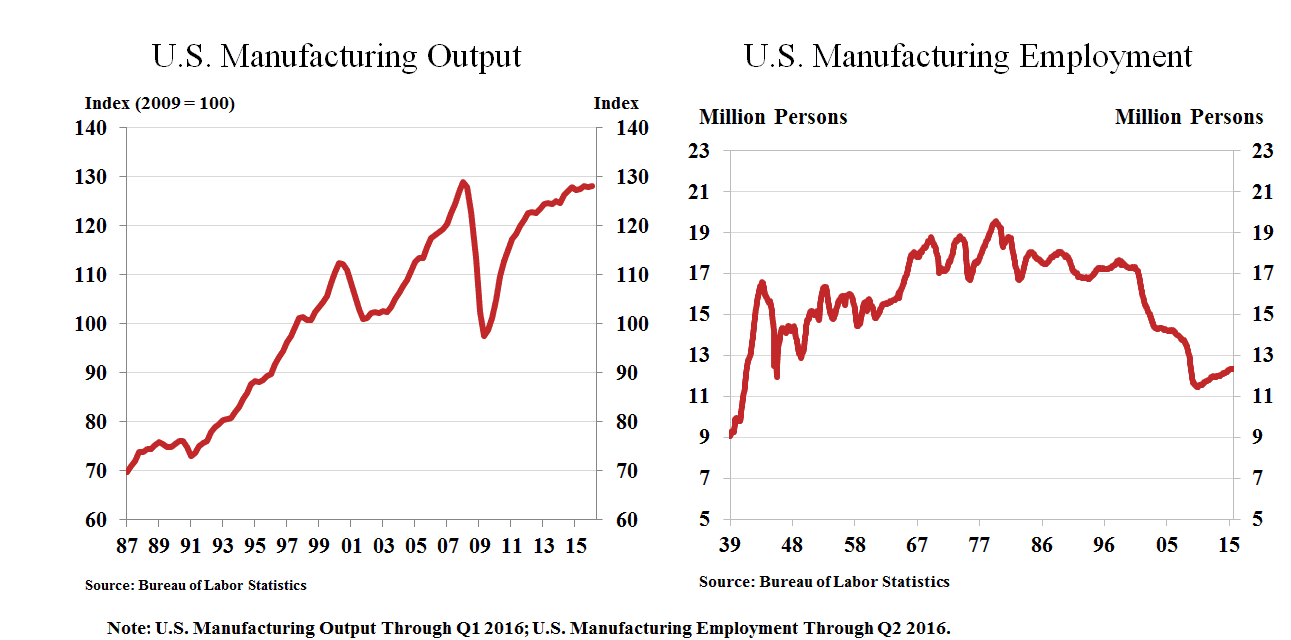

The U.S manufactures 60% more today than it did in the late 1980s, but uses 30% fewer workers. There are genuine fears that the next wave of technological innovation will be even more devastating to jobs, replacing computer-assisted manufacturing with fully computerized manufacturing; this transition has already begun.

Monetary policy, fiscal policy, government deficits and debt

Global monetary policy has prevented the world from slipping into a depression. However, low, even negative, rates are squeezing risk premiums and hindering lending. There is evidence that savings are rising to offset low rates. This has resulted in inflation of risk assets strengthening the US dollar and creating capital constraints in developing economies.

Fiscal policy needs to work in conjunction with monetary policy, but a lack of coordination within government and between governments has prevented this. Growing government deficits, due to rising healthcare and pension costs, have increased government debt. In turn, growing government debt has weighed on productive investments and wage growth.

Global growth forecast to remain lackluster

“Sub-par global economic growth, characterized by high unemployment, low inflation and interest rates. Advanced economies’ growth weighed down by structural changes, surplus labor, and ageing populations. Developing economies are likely to face capital constraints, as they are also weighed down by slower growth from advanced economies.”

Campaign policies relevant to commodity markets

CPM identify several key campaign policies that, if implemented, will have an impact on commodity markets, including—in the area of trade—the imposition of tariffs, the renegotiation of NAFTA, a reevaluation of the EU/Britain US relationship, and rejection of the Trans-Pacific Partnership, from which the new President has already removed the U.S. The new Administration has also advocated a fiscal stimulus, as well as a curb on both illegal immigration and legal immigration for temporary, low skilled workers. The Trump Administration has also signalled a change in direction on both climate change and energy policy.

Indeed, since taking office, the White House has placed a temporary ban on new rule-making by federal agencies, after which the removal of two current regulatory rules will be required to be removed for any new rule implemented. The Administration has already started its efforts to roll back and repeal Dodd Frank legislation, which include its non-conflict materials regulations, although it is not yet clear how soon, or how much of the legislation gets changed, and to what extent the non-conflict materials regulations will shape up.

Ability to implement

Following the Inauguration, President Trump did not waste any time getting started on his mission, however CPM predicts that some of the tough actions on trade, infrastructure, immigration and climate change will face hurdles in Congress, regulatory agencies and in the courts. Differences in policy approach between the President and his cabinet picks will also need to be resolved.

What do these policies mean for the world economy?

CPM anticipates that trade restrictions in the form of tariffs, the break up of existing trade pacts, and abstaining from making new pacts are likely to weigh on global economic growth. They point to a strong correlation between trade, GDP, and employment. Global Trade accounted for around 58% of Global GDP in 2015. CPM sees the impact of trade restrictions on both domestic and global growth being a negative one.

Across-the-board tariffs are, they predict, in practice impossible. There exists the danger that import tariffs will hurt U.S. manufacturers, who draw from global supply chains. CPM also warns that in the event of trade restrictions being implemented, there may be a risk to imports of critical raw materials. If, however, barriers for U.S. exports to overseas markets are brought down, this could support growth.

Fiscal Stimulus

A fiscal stimulus has been promised by President Trump, to come in the form of tax cuts—particularly on higher earners and corporations—and infrastructure spending. There is unlikely to be great resistance from Congress to tax cuts, CPM believes, and fears, that much of the additional money will not be invested in U.S. business and jobs, but would instead end up being invested in the stock market, corporate stock buy-backs, higher yielding speculative bonds, Treasuries, and offshore holdings, which are estimated at around $21 trillion. In their view, the impact of tax cuts would be inflation of risk assets and a stronger dollar.

With regard to infrastructure spending, while a promising prospect for stronger growth, plans for how to finance the spending are yet to be announced. CPM warns that if infrastructure spending is pursued with deficit financing, it will further add to U.S. debt, which would meet opposition in Congress. On the other hand, private capital investments into infrastructure projects could be made possible by removing policy bottlenecks or offering tax incentives.

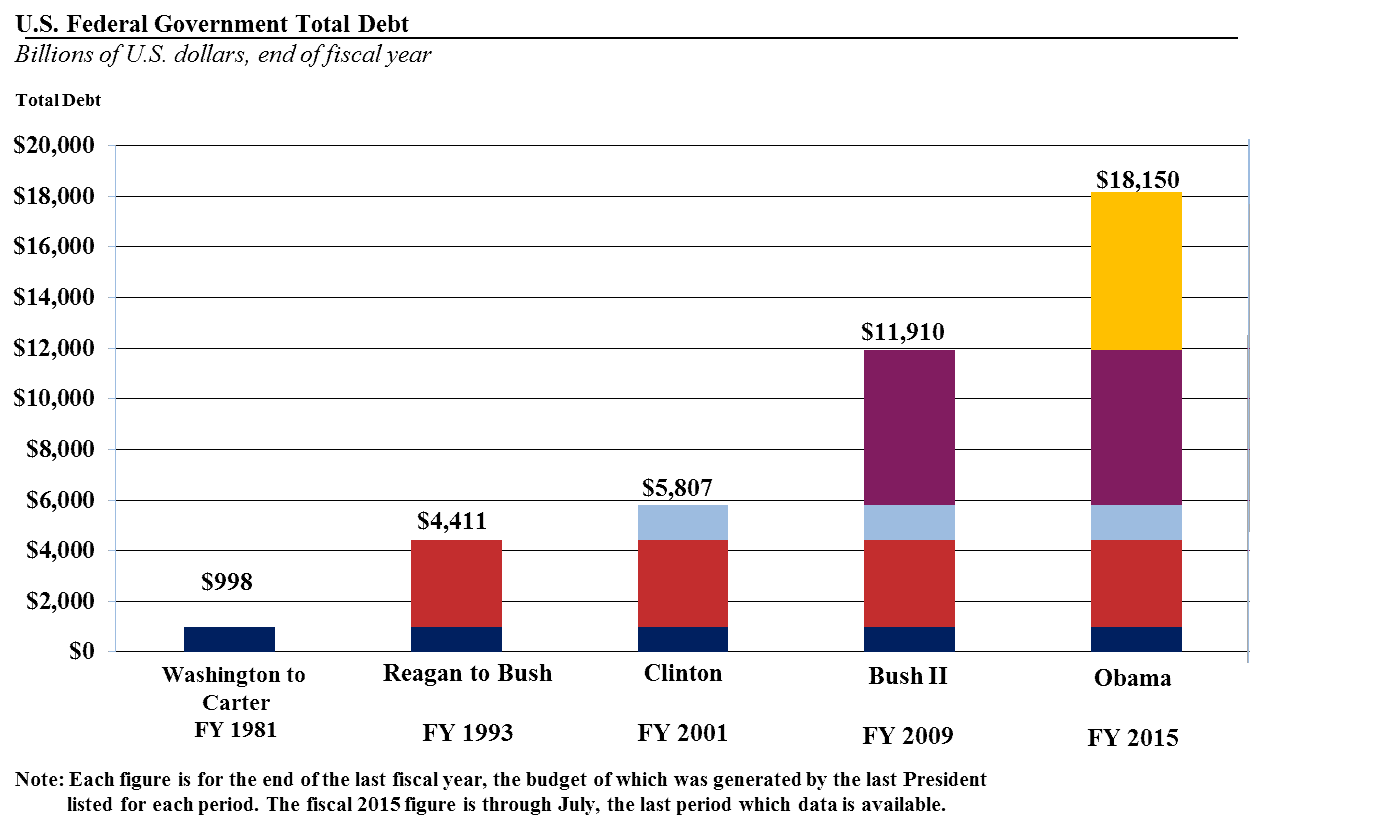

The Growth of Federal Debt

CPM’s assessment is that with governments continuing to crowd consumers, small businesses, and banks out of the credit market, the current misallocation of credit to less productive applications retards general economic growth, which in turn leads to a further extension of the era of low interest rates. At some point this should revert to more typical interest rate market patterns, but the reversion could be many years away. When it occurs, it could bring with it increased economic volatility, unless central banks and finance ministers are far more adept and agile in managing the transition than seems likely at present.

Immigration, climate change and energy

Immigration has been a major focal point of several recent campaigns. In the US, President Trump has already increased deportation of illegal immigrants, and is working on reducing or eliminating temporary/seasonal agricultural work visas. And indeed, one of his first acts as President was to implement a travel ban on those entering the country from several countries. He is also implementing a requirement that all jobs at all skill levels in the U.S. be offered to U.S. citizens or permanent legal residents before being given to a foreign worker. Outside of the U.S., the Brexit vote was largely predicated on a desire to control immigration into the UK, not to mention the impact this issue is likely to have in elections across Europe later in the year.

The impact of cuts to low skilled and seasonal immigration in the U.S. is, in the view of CPM, initially expected to drive up the cost of labor, In the longer term, however, these cuts will arguably encourage and accelerate the use of machines and computers, where possible, to replace those lower skilled jobs, so not necessarily resulting in job creation.

On the environment, there are plans to cancel the U.S. commitment to the Paris Agreement and U.S. Climate Change Fund, as well as lift restrictions on U.S. energy production.

CPM’s conclusion is that these policies, if fully implemented, are likely to have a temporary positive impact, but over the longer term are expected to have a neutral to negative impact on both U.S. as well as global GDP. It should be noted that the impacts stated above are based on the potential to deliver on campaign promises. In reality, as previously mentioned, most of these campaign promises will face significant hurdles at various levels before becoming law.

What These Policies Mean for the Commodities Markets

The U.S. dollar is expected to remain firm and possibly rise in the future, with increased demand for dollars in response to a U.S. fiscal stimulus. The currency is supported by Federal policy, in contrast to other major central banks’ loose monetary policies. In addition to strength in the dollar, for the above-mentioned reasons, key exporters to the U.S. may potentially need to devalue their currencies to overcome U.S. import tariffs, if these are indeed introduced. Figures suggested include 45% on imports from China; 35% on imports from Mexico; and 20% on all imported goods. On the other hand, a stronger dollar will make exports from the U.S. relatively uncompetitive, opening opportunities for other exporting countries.

Energy Commodities

On the supply side, CPM predicts that supply of energy commodities is likely to increase as America works on removing production restrictions presently in place. This domestic increase is likely to be matched by other countries, who are unlikely to reduce supply in any meaningful way for fear of losing market share, not to mention the fact that fuel is often the largest revenue generator for some of these countries.

CPM points to three factors impacting demand: firstly, technical innovations aimed at reducing per unit energy usage and shifting the source of required energy to electricity indicate a move away from oil and coal and towards renewables; secondly, climate change agreements are likely to proceed with or without the U.S.; and thirdly, demand will be driven by global GDP, which is expected to be lackluster.

Base and Specialty Metals

The supply of base and specialty metals is likely to be vulnerable to short-term production cuts and long-term restrictions in capacity. It is likely, in CPM’s opinion, to be market factors, as opposed to trade restrictions, which will limit supplies. They point to the fact that a number of metals (Pb, Zn, and some specialty metals) have relatively thin stock buffers.

On the demand side, technical innovations will be a factor; the substitution of specialty metals can happen over time, particularly at higher price levels. New applications, including in batteries, solar power generation, LCD etc will see the growth of certain specialty metals. Additionally, upgrades in residential consumptions of specialty steels in developing economies may drive demand higher over the next decade.

Recovery of the oil & gas sector, and capital spending on related infrastructure are also highlighted as being key to near-term growth.

The MMTA warmly thanks Mu Li and CPM for taking the time to share its outlook with MMTA members. It would not be an exaggeration to say that there was an animated response from the room from attendees with a more positive view of future developments under President Trump, and the key appears to be the balance between campaign rhetoric and the laws ultimately enacted following the scrutiny of government and the courts, not to mention the impact of both international and domestic public pressure.

CPM Group (www.cpmgroup.com) has pioneered fundamental and econometric research in commodities with a focus on specialty metals. CPM Group’s research program was started in the 1970s, based on the view that metals and other commodities markets were highly asymmetrical, poorly reported and understood by many market participants, and often clouded by misinformation and false assumptions about the nature of these markets. CPM Group uses micro-economic analysis of the individual components of each commodity market, wedded with a top-down macro-economic analysis of the global trends affecting these markets.

Mu Li is CPM Group’s Director of Base and Specialty Metals Research & Senior Precious Metals Analyst. Ms. Li has researched extensively on markets and industries of base, specialty, and precious metals, focusing on supply and demand fundamentals, policy developments, as well as investment-related issues related to these sectors. She manages CPM Group’s research projects related to base and specialty metals, and regularly contributes analysis on commodity markets and industries, the financial markets, and economic conditions. Ms. Li was previously a reporter at Platts, a division of McGraw Hill Financial, where she covered businesses and regulations in the energy and metals sectors, and has been a White House Correspondents Association scholar.

The post MMTA Inauguration-Eve Outlook on Trump, Trade & Commodities appeared first on MMTA.